Dear Investor,

When we think about investing there are a few common topics that come to mind, such as diversification, valuations, interest rates, returns and growth rates, to name a few. While these are all important, we believe the key factor with the greatest impact on long term outcomes, is investor behaviour – how investors react during various market cycles.

But isn’t Behavioural Finance already a thing?!

While investors have lately started to embrace the importance of Psychology in investing and financial decisions, we think that there is a lot more that can be done. For example: the most common investment approach amongst financial advisors is “Buy good business and Hold.” Using this approach, the financial advisor helps an investor select an asset allocation, makes slight modifications over time, but primarily recommends investors ‘stay the course.’ We are not suggesting that this strategy isn’t fairly effective in theory, however, in reality investors tend to capitulate when the market suffers a correction; so, the question is not so much about the effectiveness of the strategy, but an investors ability to follow it.

Exhibit 1: Investment return >> Investor Return… and the difference is Behaviour Gap

Source: Carl Richards’s book: The Behaviour Gap, Ambit Asset Management

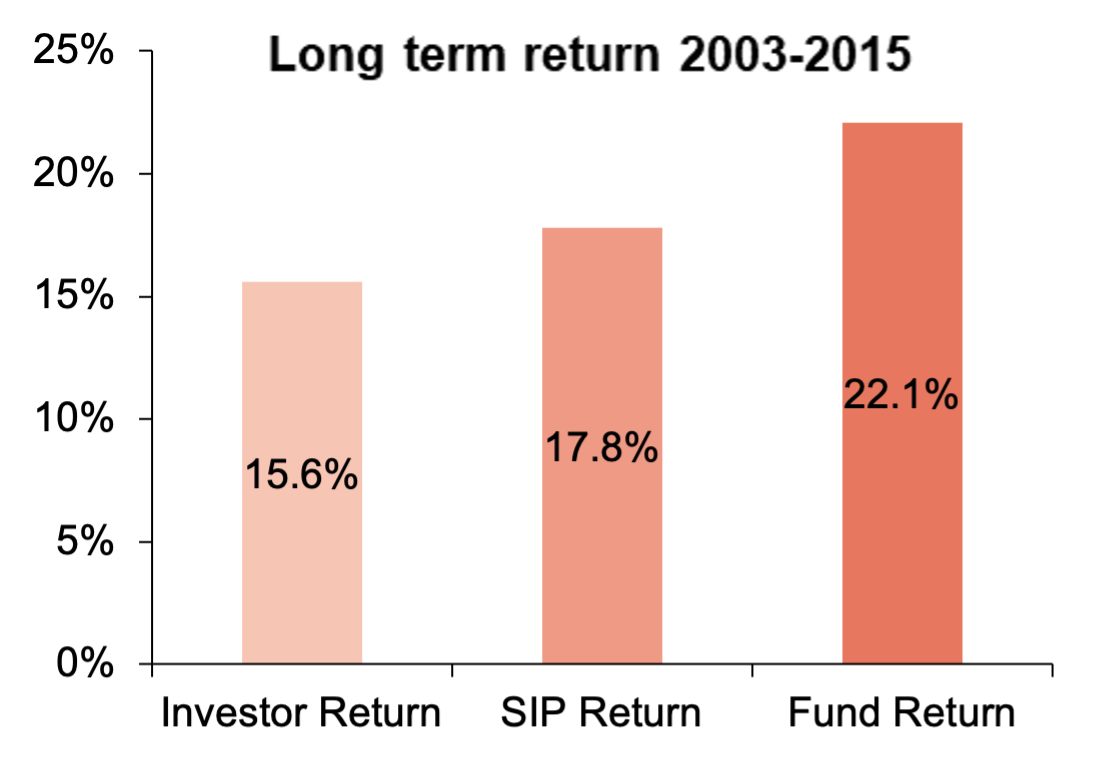

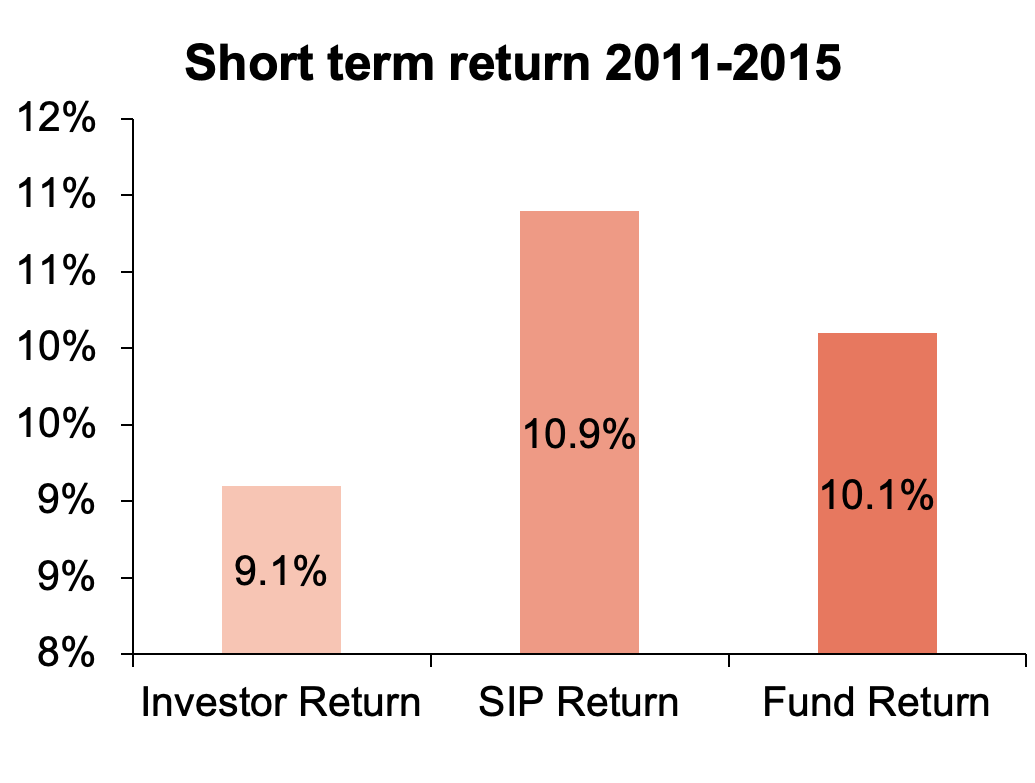

In a study on Investor Behaviour from 2003-2015 Axis MF analysed the returns earned by the investors compared to their Fund (NAV) returns. Interestingly, Investors’ realized returns were significantly lower as compared to their respective fund performance during that period. This was due to volatile investment flows by investor which tend to follow market performance, as compared to disciplined lump-sum (Buy-and-Hold) or SIP investments.

Our broad investment philosophy is of identifying resilient businesses, limiting churn and remaining invested in them for the longer duration and let compounding work its magic – Time IN the market rather than TIMING the market. We highlighted the same in our Coffee Can philosophy note.

Exhibit 2: Long Term comparison of Investment vs Investor returns in Equity Funds from 2003-2015

Source: Ambit Asset Management, Axis MF Study

Exhibit 3: Short Term (5 yr) comparison of Investment vs Investor returns in Equity Funds from 2011-2015

Source: Ambit Asset Management, Axis MF Study

…and what to do about it?

Money and emotions are intrinsically linked. Investors are slowly realising how behaviour is the most dominant factor in investor returns and just how unconscious we humans are of our own blind spots and biases. We – as investors – are terrible at knowing ourselves and knowing when we’re being led by our own prejudiced thinking. When it comes to investing, investors often tend to focus on market timing and short-termism, fed by the media and the world wanting to sell to you. While we understand asset allocation, fund choice, returns etc. are all important, however ultimately, an investor’s awareness of these behavioural biases and cognizance of blind spots, go a long way in determining the ultimate results importance of investing behaviour is what really counts. In this newsletter, we highlight some common behavioural biases which investors usually face while not being cognizant of the same.

JP Morgan’s research in their Annual Guide to the Markets, reports that behaviour is the most influential factor in an individual investment success or failure, representing a 70% contribution to investor returns.

Behavioural Finance! What is it & how is it impacting your investments??

Behavioural Finance is an area of study looking at the relationship between behavioural psychology and conventional finance, and ultimately seeks to understand the driving forces behind irrational financial decisions. It focuses on the fact that investors are not always rational, have limits to their self-control, and are influenced by their own biases.

So, which behaviours have the most detrimental impact on your finances and which are you suffering from? There are a lot we could discuss, but here are a few:

1. Confirmation Bias

Confirmation bias is the tendency of people to pay close attention to information that confirms their belief and ignore information that contradicts it.

For example: If someone believes strongly that Spinach is good for their health, they are quite likely to find information online that confirms their beliefs and vice-versa. The same goes for investing. If there is a particular stock or fund that we believe will do well in the upcoming years, we may be more inclined to find information to support our conclusion, than to discredit it.

Confirmation bias can very easily create tunnel vision. Not only could this result in investing in something subpar, it could also mean missing out on other good investment opportunities.

Are you aware of the echo chamber you’ve built for yourself?

2. Anchoring bias:

It can be seen in investing when we value a stock based on what we paid for it – the price – or relative to a specific event such as All Time High or All Time Low, rather than paying attention to the fundamentals. Anchoring means that the framework for interpreting and analysing the available information can be influenced disproportionately by an initial, default position or “anchor.” This anchor can be chosen in a variety of ways.

For example: If I were to ask you where you think HDFC Bank’ stock will be in three months, how would you approach it? Many people would first say, “Okay, where’s the stock today?” Then, based on where the stock is today, they will make an assumption about where it’s going to be in three months. That’s a form of anchoring bias. We’re starting with a price today, and we’re building our sense of value based on that anchor.

Exhibit 4: Historically Investors tend to buy and sell based on the recent performance of the market

Source: AMFI, Ambit Asset Management

3. Hindsight Bias

Hindsight is a beautiful thing, but if only we knew then, what we know now. Regret is the feeling that an opportunity has been missed, and is typically an expression of hindsight bias.

Everything is clear with the benefit of hindsight and yet we often beat ourselves up anyway over decisions we made. It’s important to not let hindsight bias cloud our minds when investing. Simply put, there is no way we could have known what would have played out, how it would have occurred, or when it would have happened.

For example, after attending a baseball game, you might insist that you knew that the winning team was going to win beforehand

However, we sometimes convince ourselves that we could have predicted it; therefore we attempt to use past events to try to predict future events. And we all know how horribly that can end!

4. Self-attribution Bias

People often take credit for successes and blame others / external factors for failures, which is typical of self-attribution bias. In other words, success is attributed to the individual’s skill, while failures are attributed to external factors or luck. Illusion of knowledge and self-attribution biases, in-turn – contribute to the overconfidence bias.

For example: Athletes win a game and attribute their win to hard work and practice. When they lose game, they blame the loss on bad calls by the referees.

The self-attribution serving bias is unique in that it is closely related to our self-esteem. But knowing how to admit when you are in the wrong or are responsible for a negative outcome is paramount to growth, it’s important to challenge the self-serving bias and learn how to be better at taking criticisms to improve decision making.

5. Fear of Missing Out (FOMO)

One word — Gamestop. If you never heard about that fiasco, you should try Google it. It’s a prime example of the dangers of FOMO

In recent years, investing has become increasingly accessible to the masses. The barriers to entry are lower than ever, a myriad of sleek and easy-to-use investing apps are hitting the markets, and the internet is flooded with people sharing what they think is ‘the next big thing’.

Undoubtedly, there are positive aspects to the changing landscape of the investing world. However, the noise created around the “hottest stocks & funds” can create a false sense of urgency that if you don’t invest in that particular thing now, you could be missing out on the chance to make a fortune.

Exhibit 5: Investors often tend to buy high (Greed) & sell low (Fear) and miss on compounding returns

Source: Benjamin Talin, More than digital Ambit Asset Management

6. Herd Mentality:

Herd behaviour happens when investors follow others rather than making their own decisions based on financial data. Going against the crowd (or non-conformity) typically triggers fear in people immediately. Why? Because everyone saying “ABC ltd is highly valued” makes them fear that they might be wrong in thinking “ABC ltd may NOT be expensively values”. They additionally may fear being embarrassed or appearing foolish if they go ahead with their choice, and more so if it turns out to be wrong.

For example, if all your friends are investing in penny stocks, you might start too even though it's risky.

Herd behaviour can backfire. It can create massive bubbles like the Dutch tulip market bubble, the Dot-Com bubble, even the real estate bubble of the mid-2000s & Crypto market... and bubbles burst.

7. Loss aversion bias:

It is a tendency in behavioural finance where investors are so fearful of losses that they focus on trying to avoid a loss more than on making gains.

Research on loss aversion shows that investors feel the pain of a loss more than twice as strongly as they feel the enjoyment of making a profit. For example, the pain of losing Rs 100 is often far greater than the joy gained in finding the same amount.

A disciplined approach to investment based on fundamental analysis is a good way to alleviate the impact of the loss-aversion Bias. It is impossible to make experiencing losses any less painful emotionally but analysing investments and realistically considering the probabilities of future losses and gains may help in improving rational decisions.

Conclusion: The Future of Behavioural Finance

Our fund managers often emphasise on the importance of EQ (Emotional Quotient) and SQ (Social Quotient) over IQ (Intelligence Quotient). As you can probably tell, it is really difficult to separate psychology from financial decision-making. An increased understanding and awareness of these behavioural biases will improve awareness regarding the emotional factors and psychological processes of investors & discover effective ways to let psychology lead investors to better choices regarding finances!

To read more about investor behaviour one may refer the following books:

- The Behaviour Gap – Book by Carl Richards

- Thinking, Fast and Slow – Book by Daniel Kahneman

- The Psychology of Money – Book by Morgan Housel

- Beyond Greed and Fear – Book by Hersh Shefrin

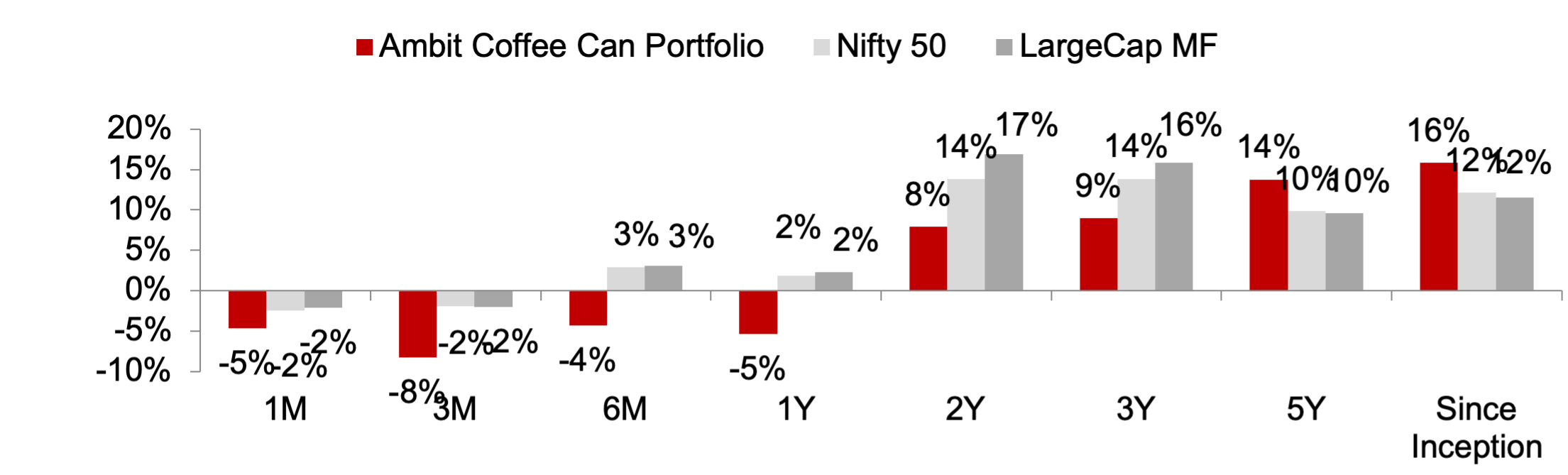

Ambit Coffee Can Portfolio

At Coffee Can Portfolio, we do not attempt to time commodity/investment cycles or political outcomes and prefer resilient franchises in the retail and consumption-oriented sectors. The Coffee Can philosophy has unwavering commitment to companies that have consistently sustained their competitive advantages in core businesses despite being faced by disruptions at regular intervals. As the industry evolves or is faced by disruptions, these competitive advantages enable such companies to grow their market shares and deliver long-term earnings growth.

Exhibit 6: Ambit’s Coffee Can Portfolio point-to-point performance

Source: Ambit; Portfolio inception date is March 6, 2017; Returns as of 31st Aug, 2022; All returns are post fees and expenses; Returns above 1-year are annualized; Note: Returns prior to Apr’19 are returns of all the Pool accounts excluding non-aligned portfolio, and returns post Apr’19 is based on TWRR returns of all the pool accounts.

Exhibit 7: Ambit’s Coffee Can Portfolio calendar year performance

Source: Ambit; Portfolio inception date is March 6, 2017; Returns as of 31st Aug, 2022; All returns are post fees and expenses. Note: Returns prior to Apr’19 are returns of all the Pool accounts excluding non-aligned portfolio, and returns post Apr’19 is based on TWRR returns of all the pool accounts.

Ambit Good & Clean Midcap Portfolio

Ambit's Good & Clean strategy provides long-only equity exposure to Indian businesses that have an impeccable track record of clean accounting, good governance, and efficient capital allocation. Ambit’s proprietary ‘forensic accounting’ framework helps weed out firms with poor quality accounts, while our proprietary ‘greatness’ framework helps identify efficient capital allocators with a holistic approach for consistent growth. Our focus has been to deliver superior risk-adjusted returns with as much focus on lower portfolio drawdown as on return generation. Some salient features of the Good & Clean strategy are as follows:

- Process-oriented approach to investing: Typically starting at the largest 500 Indian companies, Ambit's proprietary frameworks for assessing accounting quality and efficacy of capital allocation help narrow down the investible universe to a much smaller subset. This shorter universe is then evaluated on bottom-up fundamentals to create a concentrated portfolio of no more than 20 companies at any time.

- Long-term horizon and low churn: Our holding horizons for investee companies are 3-5 years and even longer with annual churn not exceeding 15-20% in a year. The long-term orientation essentially means investing in companies that have the potential to sustainably compound earnings, with this compounding earnings acting as the primary driver of investment returns over long periods.

- Low drawdowns: The focus on clean accounting and governance, prudent capital allocation, and structural earnings compounding allow participation in long-term return generation while also ensuring low drawdowns in periods of equity market declines.

Exhibit 8: Ambit’s Good & Clean Midcap Portfolio point-to-point performance

Source: Ambit; Portfolio inception date is March 12, 2015; Returns as of 31st Aug, 2022; All returns above 1 year are annualized. Returns are net of all fees and expenses

Exhibit 9: Ambit’s Good & Clean Midcap Portfolio calendar year performance

Source: Ambit; Portfolio inception date is March 12, 2015; Returns as of 31st Aug, 2022. Returns are net of all fees and expenses

Ambit Emerging Giants Portfolio

Smallcaps with secular growth, superior return ratios and no leverage –Ambit's Emerging Giants portfolio aims to invest in small-cap companies with market-dominating franchises and a track record of clean accounting, governance and capital allocation. The fund typically invests in companies with market caps less than Rs4,000cr. These companies have excellent financial track records, superior underlying fundamentals (high RoCE, low debt) and ability to deliver healthy earnings growth over long periods of time. However, given their smaller sizes, these companies are not well discovered, owing to lower institutional holdings and lower analyst coverage. Rigorous framework-based screening coupled with extensive bottom-up due diligence lead us to a concentrated portfolio of 15-16 emerging giants.

Exhibit 10: Ambit Emerging Giants Portfolio point-to-point performance

Source: Ambit; Portfolio inception date is December 1, 2017; Returns as of 31stAug, 2022; All returns above 1 year are annualized. Returns are net of all fees and expenses

Exhibit 11: Ambit Emerging Giants Portfolio calendar year performance

Source: Ambit; Portfolio inception date is December 1, 2017; Returns as of 31stAug, 2022. Returns are net of all fees and expenses

Ambit TenX Portfolio

Ambit TenX Portfolio gives investors an opportunity to participate in the India growth story as the Indian GDP heads towards a US$10tn mark over the next 12-15 years. Mid and Small corporates are expected to be the key beneficiaries of this growth. The portfolio intends to capitalize on this opportunity by identifying and investing in primarily mid & small cap companies that can grow their earnings 10x over the same period implying 18-21% CAGR. Key features of this portfolio would be as follow:

- Longer-term approach with a concentrated portfolio: Ideal investment duration of >5 years with 15-20 stocks.

- Key driving factors: Low penetration, strong leadership, light balance sheet

- Forward-looking approach: Relying less on historical performance and more on future potential while not deviating away from the Good & Clean philosophy.

- No Key-man risk: Process is the Fund Manager

Exhibit 12: Ambit TenX Portfolio point-to-point performance

Source: Ambit; Portfolio inception date is December 13, 2021; Returns as of 31stAug, 2022; Returns are net of all fees and expenses

Exhibit 13: Ambit TenX Portfolio calendar year performance

Source: Ambit; Portfolio inception date is December 13, 2021; Returns as of 31stAug, 2022. Returns are net of all fees and expenses

For any queries, please contact:

Umang Shah- Phone: +91 22 6623 3281, Email - [email protected]

Ambit Investment Advisors Private Limited - Ambit House, 449, Senapati Bapat Marg, Lower Parel, Mumbai - 400 013

Risk Disclosure & Disclaimer

The performance of the Portfolio Manager has not been approved or recommended by SEBI nor SEBI certifies the accuracy or adequacy of the performance related information contained therein.

Ambit Investment Advisors Private Limited (“Ambit”), is a registered Portfolio Manager with Securities and Exchange Board of India vide registration number INP000005059.

This presentation / newsletter / report is strictly for information and illustrative purposes only and should not be considered to be an offer, or solicitation of an offer, to buy or sell any securities or to enter into any Portfolio Management agreements. This presentation / newsletter / report is prepared by Ambit strictly for the specified audience and is not intended for distribution to public and is not to be disseminated or circulated to any other party outside of the intended purpose. This presentation / newsletter / report may contain confidential or proprietary information and no part of this presentation / newsletter / report may be reproduced in any form without its prior written consent to Ambit. All opinions, figures, charts/graphs, estimates and data included in this presentation / newsletter / report is subject to change without notice. This document is not for public distribution and if you receive a copy of this presentation / newsletter / report and you are not the intended recipient, you should destroy this immediately. Any dissemination, copying or circulation of this communication in any form is strictly prohibited. This material should not be circulated in countries where restrictions exist on soliciting business from potential clients residing in such countries. Recipients of this material should inform themselves about and observe any such restrictions. Recipients shall be solely liable for any liability incurred by them in this regard and will indemnify Ambit for any liability it may incur in this respect.

Neither Ambit nor any of their respective affiliates or representatives make any express or implied representation or warranty as to the adequacy or accuracy of the statistical data or factual statement concerning India or its economy or make any representation as to the accuracy, completeness, reasonableness or sufficiency of any of the information contained in the presentation / newsletter / report herein, or in the case of projections, as to their attainability or the accuracy or completeness of the assumptions from which they are derived, and it is expected each prospective investor will pursue its own independent due diligence. In preparing this presentation / newsletter / report, Ambit has relied upon and assumed, without independent verification, the accuracy and completeness of information available from public sources. Accordingly, neither Ambit nor any of its affiliates, shareholders, directors, employees, agents or advisors shall be liable for any loss or damage (direct or indirect) suffered as a result of reliance upon any statements contained in, or any omission from this presentation / newsletter / report and any such liability is expressly disclaimed. Further, the information contained in this presentation / newsletter / report has not been verified by SEBI.

You are expected to take into consideration all the risk factors including financial conditions, risk-return profile, tax consequences, etc. You understand that the past performance or name of the portfolio or any similar product do not in any manner indicate surety of performance of such product or portfolio in future. You further understand that all such products are subject to various market risks, settlement risks, economical risks, political risks, business risks, and financial risks etc. and there is no assurance or guarantee that the objectives of any of the strategies of such product or portfolio will be achieved. You are expected to thoroughly go through the terms of the arrangements / agreements and understand in detail the risk-return profile of any security or product of Ambit or any other service provider before making any investment. You should also take professional / legal /tax advice before making any decision of investing or disinvesting. The investment relating to any products of Ambit may not be suited to all categories of investors. Ambit or Ambit associates may have financial or other business interests that may adversely affect the objectivity of the views contained in this presentation / newsletter / report.

Ambit does not guarantee the future performance or any level of performance relating to any products of Ambit or any other third party service provider. Investment in any product including mutual fund or in the product of third party service provider does not provide any assurance or guarantee that the objectives of the product are specifically achieved. Ambit shall not be liable for any losses that you may suffer on account of any investment or disinvestment decision based on the communication or information or recommendation received from Ambit on any product. Further Ambit shall not be liable for any loss which may have arisen by wrong or misleading instructions given by you whether orally or in writing. The name of the product does not in any manner indicate their prospects or return.

The product ‘Ambit Coffee Can Portfolio’ has been migrated from Ambit Capital Private Limited to Ambit Investments Advisors Private Limited. Hence some of the information in this presentation may belong to the period when this product was managed by Ambit Capital Private Limited.

You may contact your Relationship Manager for any queries.

The performance data for coffee can product between 6th march 2017 - 19th June 2017 represents model portfolio returns. First client was onboarded on 20th June 2017. The performance data for G&C product between 1st June 2016 to 1st April 2018 also includes returns for funds managed for an advisory offshore client. Returns are calculated using TWRR method as prescribed under revised SEBI (Portfolio Managers) Regulations, 2020.